For Prepared Investors, Market Downturns are a Tremendous Opportunity

Many investors seek investment advice during market downturns and volatility due to anxiety and uncertainty about the future. The prudent path, assuming you have a formal financial plan and road map in place, is to stay the course. Sometimes it's hard to follow that advice when you are witnessing your portfolio losing value.

It seems everywhere you turn--financial shows, friends or colleagues--there are all sorts of advice regarding what to do now!

Financial markets are cyclical, and every market goes through a growth, maturity and decline cycle. No matter what state we are in, it is wise for one to take a deep breath, get a hold of real facts and data, and revisit their financial plan so that they are able to have the confidence that this time is not different from any other cycle that investors have experienced since the dawn of investing.

Let's dive in and talk about market downturns and how you can be better prepared cognitively and emotionally when things seem uncertain.

It all starts with a financial road map - the financial plan is your guide

A financial plan is more than a spreadsheet with projections and numbers. It's a roadmap for your future, and once you have one, it can help you make better-informed decisions about your money and not get caught up in the emotions of the market.

A good financial plan is a road map that is customized to your needs, goals, and values. It's not something that can be done in 20 minutes online or by filling out a form on the back of an envelope like some form at the doctor's office. It's a customized solution developed specifically for you—and it takes into account any market cycle that comes your way.

Like any good road map, it doesn't tell you exactly where to go but rather sets out options for how best to get where you want to go given current circumstances (like traffic conditions) as well as long-term objectives (like wanting ample funds in retirement).

A well-designed financial plan takes into account all aspects of an individual’s life—retirement savings plans; taxes; insurance coverage; education funding for children or grandchildren; charitable giving goals—and helps ensure that all parts align with each other so no piece of the puzzle gets left behind when making big financial decisions.

Let's Look at some real numbers

Since 2000, there have been three distinct bear markets:

The Dot-Com Bubble Burst - March 2000-October 2002

The Global Financial Crisis - October 2007-March 2009

The Covid-19 Crash - February 2020-March 2020

What is considered a Bear Market?

A bear market is when the stock market drops by at least 20% from its previous high. Investopedia writes: "A bear market is when a market experiences prolonged price declines. It typically describes a condition in which securities prices fall 20% or more from recent highs amid widespread pessimism and negative investor sentiment. Bear markets are often associated with declines in an overall market or index like the S&P 500, but individual securities or commodities can also be considered to be in a bear market if they experience a decline of 20% or more over a sustained period of time—typically two months or more."

Investor's are their own worst enemy when it comes to trying to market volatility

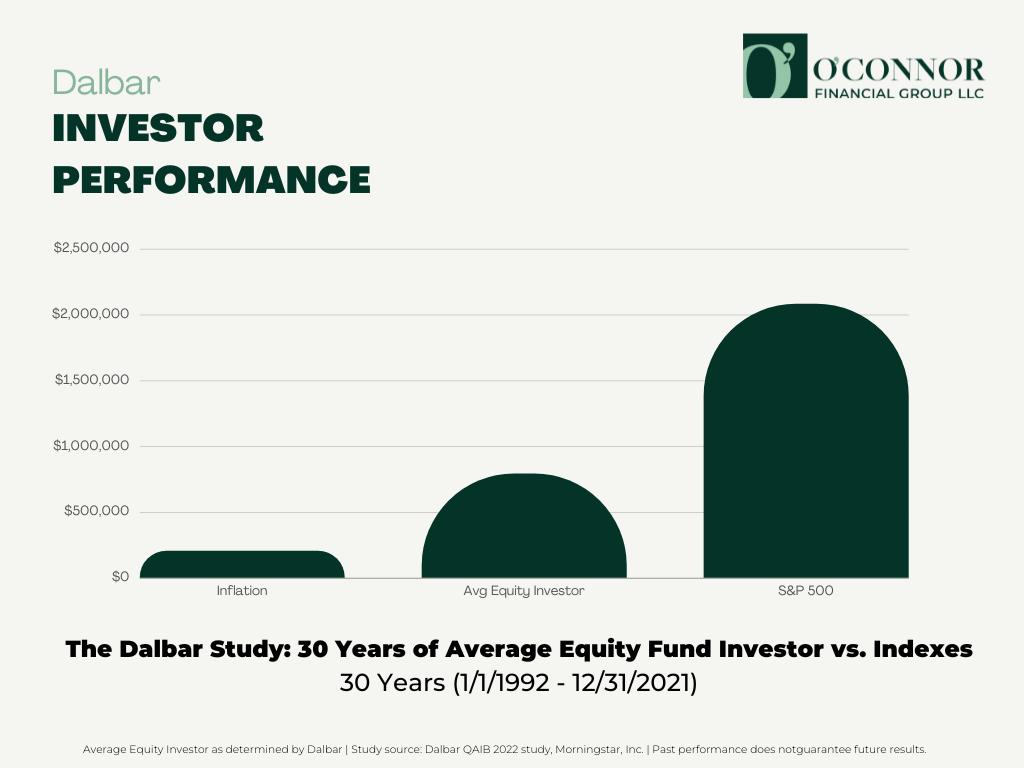

Independent investment research institute DALBAR has been tracking investor behavior since 1994. DALBAR publishes yearly findings in their report called Quantitative Analysis of Investor Behavior (QAIB). The QAIB reports measures "the effects of investor decisions to buy, sell and switch into and out of mutual funds over short and long-term timeframes. These effects are measured from the perspective of the investor and do not represent the performance of the investments themselves. The goal of QAIB is to improve performance of both independent investors and financial advisors by managing behaviors that cause investors to act imprudently." Simply, the QAIB measures how investors fare in all sorts of markets.

In 2021, DALBAR released a twenty-year study comparing the average equity investor and the S&P 500 index. Here are the findings (see chart below):

During this period, the average equity fund investor has fallen behind the S&P 500 Index—which represents large company stocks in the U.S.—as a result of trying to outguess markets.

Bear Market Returns and Investor Behavior

The Dot-Com Bubble Burst

During the The Dot-Com Bubble Burst - March 2000-October 2002 the market melted with losses in the NASDAQ Tech index losing two-thirds of its value by October 2002. The S&P 500 Index was down over 21% during this period. Naturally, many investors exited the market in a panic trying to cut their losses.

The Investment Company Institute tracks inflows and outflows of investment dollars. The reports of 2000-2002 indicate investors fleeing stock equities. You can read the detailed report here.

The Global Financial Crisis of 2007-2009

It was the same story for investors in the Global Financial Crisis of October 2007-March 2009. A global financial crisis was triggered by a downturn in U.S. housing prices with a bear market that saw the S&P 500 down 57%. The subprime mortgage crisis, which originated in the United States but quickly spread around the world, sparked a global financial meltdown. At the time, it was the “worst economic downturn since the recession of 1937-38.” (Investopedia)

Robert Rich of the Federal Reserve Bank of Cleveland wrote regarding this global crisis: "The Great Recession began in December 2007 and ended in June 2009, which makes it the longest recession since World War II. Beyond its duration, the Great Recession was notably severe in several respects. Real gross domestic product (GDP) fell 4.3 percent from its peak in 2007Q4 to its trough in 2009Q2, the largest decline in the postwar era (based on data as of October 2013). The unemployment rate, which was 5 percent in December 2007, rose to 9.5 percent in June 2009, and peaked at 10 percent in October 2009. The financial effects of the Great Recession were similarly outsized: Home prices fell approximately 30 percent, on average, from their mid-2006 peak to mid-2009, while the S&P 500 index fell 57 percent from its October 2007 peak to its trough in March 2009. The net worth of US households and nonprofit organizations fell from a peak of approximately $69 trillion in 2007 to a trough of $55 trillion in 2009. As the financial crisis and recession deepened, measures intended to revive economic growth were implemented on a global basis. The United States, like many other nations, enacted fiscal stimulus programs that used different combinations of government spending and tax cuts. These programs included the Economic Stimulus Act of 2008 and the American Recovery and Reinvestment Act of 2009."

The story for investors is the same. When bear markets hit, many panic and sell at the wrong time. The subsequent ten-year period after this bear market saw the S&P 500 return close to 14%. Dalbar once again proved its long-standing thesis: the 20-year period that ended Dec. 31, 2009 saw the average investment return at 8.20% percent while the Average equity investor return at 3.17% percent.

The Covid-19 Crash - February 2020-March 2020

Most recently, investors experienced market volatility in a matter of a few months with the COVID epidemic. From February 2020 through April 2020, the S&P 500 lost close to 20%. Investors were scared regarding the long-term impact of COVID on the economy and the market.

The financial press was filled with gloom as investors 'doom scrolled' through the crisis wondering whether or not to stay invested.

Of course, investors who stayed the course saw the market were rewarded--the S&P 500 ended the year close to 19% return.

What's the lesson regarding market downturns for investors?

First, there is market uncertainty with investing. No one can reliably and predictably forecast what the market will do going forward in the future. If someone could do that, why would they tell you? However, we can learn from the past by looking at long-term performance data not to see patterns necessarily but that markets are random and unpredictable--they reward investors who take the risk seeking a return premium. If there was not a return premium, there would be no reason to invest in stock equities (see our previous post about risk and return).

Secondly, the market rewards those who take the long-term view of investing and stay the course. From March 2000 to the end of 2021, the S&P 500 returned close to 8%. Of course, past performance is not a guarantee of future performance, but the long-term probability is in the favor of the investor who is disciplined and stays focused on their financial future.

Lastly, a financial roadmap and plan can be the guide that can help you stay the course and filter out the noise that investors are bombarded with on a daily basis. A prudent plan is a veritable roadmap since it shows you the path to take to meet your goals and dreams. The beauty of a financial plan is that it takes into account all sorts of market scenarios as well as life events to ensure you have the highest probability to have the financial peace you deserve.

If you have any questions about how to manage your emotions during market downturns or to revisit your financial plan, give us a call or contact us here.